Consumer confidence rose slightly in March but those surveyed after the Iran conflict began told a very different story. Here is what small business owners should be watching closely this month.

What’s happening: CreditorWatch chief economist Ivan Colhoun says the outlook is getting more complicated for businesses and consumers alike.

Why this matters: For small businesses already managing stretched consumer spending, rising input costs and persistent inflation, the next few weeks could bring further pressure.

The Australian economy is holding steady on the surface, but underneath, the conditions small businesses are navigating are getting more complicated. That is the assessment of CreditorWatch chief economist Ivan Colhoun, drawing on the February 2026 NAB Business Survey and the March 2026 Westpac Consumer Sentiment Survey.

For small business owners trying to read where things are heading, Colhoun points to three developments worth watching closely in the weeks ahead.

Inflation is not going away

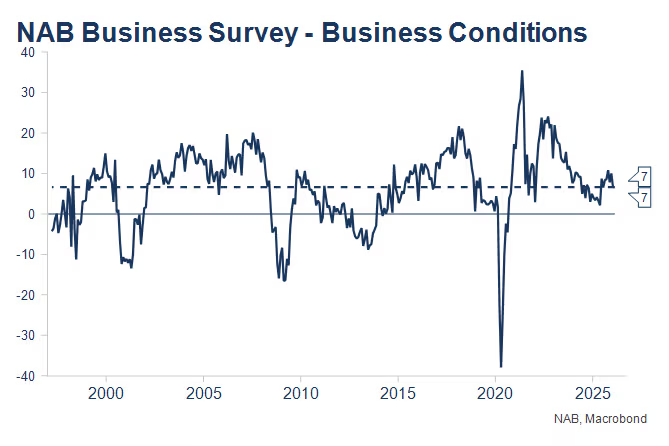

The first is inflation. Business conditions held at their long-run average of plus seven in February, but the detail inside the NAB survey is less comfortable. Capacity utilisation remained elevated at 82.8 per cent, and input cost and retail price components bounced back to levels Colhoun describes as inconsistent with the RBA’s 2.5 per cent inflation target.

The RBA’s own forecasts do not have inflation falling below three per cent until mid-2027 and not returning to near 2.5 per cent until mid-2028. Colhoun says that timeline is likely unacceptable to the RBA Board, given the significant rise in the price level since COVID and the disproportionate impact of persistent inflation on lower-income households.

“Taken alongside the RBA’s slow forecast return of inflation to target, the NAB survey strengthens the case for a further near-term rate increase, with the Board likely to seriously consider a 25bp move at next week’s meeting,” Colhoun said.

For small businesses, a further rate rise would mean higher borrowing costs and continued pressure on already stretched consumer spending.

Consumers are nervous

The second variable is consumer confidence. The Westpac Consumer Sentiment Survey showed confidence rose slightly by 1.2 per cent in March, suggesting the February rate rise had less immediate impact on households than expected. But Colhoun says the headline number masks a more concerning trend underneath.

“Consumer confidence remains in net pessimistic territory, a situation that the cost of living and inflation has brought about more or less persistently since 2022,” he said.

Westpac noted that responses collected in the latter part of the survey period were materially weaker than earlier responses, consistent with an index reading of 84, reflecting growing anxiety among consumers surveyed after the Iran conflict began. Unemployment expectations also deteriorated 3.8 per cent in March, with the decline most pronounced among those aged over 45, according to Westpac.

For small businesses reliant on consumer spending, the gap between the headline number and that later-survey reading is worth watching as the conflict develops.

Oil prices add to the pressure

The third variable is oil. The NAB survey was completed before hostilities commenced against Iran, meaning the full impact of the conflict has not yet been captured in the business conditions data. Since then, oil prices have risen by approximately US$20 to US$25 per barrel over the past eight days, a development Colhoun says will push inflation further away from target and add directly to business input costs.

“The circa US$20-25pb rise in the past eight days is unwelcome news for business and consumers as it adds further to costs at a time when consumer finances are already stretched,” Colhoun said.

For businesses with any exposure to fuel, freight or energy costs, the trajectory of oil prices in the coming weeks is the most immediate variable to monitor. How long the conflict lasts and the degree to which prices remain elevated will shape the outlook significantly, Colhoun said.

The one offset worth watching

Against these pressures, Colhoun points to one factor that has been doing important work in the background: the labour market. Low unemployment has cushioned the impact of cost-of-living pressures on consumer spending, and Colhoun says without it the implications for businesses, credit conditions and the broader economy would likely have been considerably more serious.

Unemployment expectations did deteriorate in March, and Colhoun notes the trend may be worsening again, making the jobs data one more number worth keeping an eye on in the months ahead.

For small business owners, the three things to watch most closely right now are the RBA’s decision at next week’s board meeting, the direction of oil prices as the Iran conflict unfolds, and whether consumer confidence stabilises or continues to slide in the weeks ahead.

Read full report here.

Keep up to date with our stories on LinkedIn, Twitter, Facebook and Instagram.